Gazelle District Service Improvement Program Performance Audit Report 2007-2016

Mentions of people and company names in this document

It is not suggested or implied that simply because a person, company or other entity is mentioned in the documents in the database that they have broken the law or otherwise acted improperly. Read our full disclaimer

Document content

-

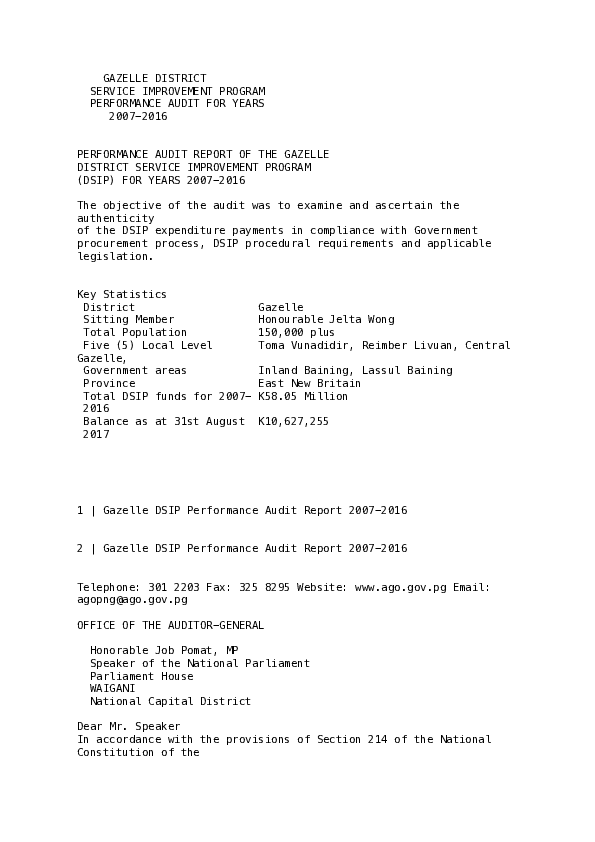

GAZELLE DISTRICT

SERVICE IMPROVEMENT PROGRAM

PERFORMANCE AUDIT FOR YEARS

2007-2016PERFORMANCE AUDIT REPORT OF THE GAZELLE

DISTRICT SERVICE IMPROVEMENT PROGRAM

(DSIP) FOR YEARS 2007-2016The objective of the audit was to examine and ascertain the

authenticity

of the DSIP expenditure payments in compliance with Government

procurement process, DSIP procedural requirements and applicable

legislation.Key Statistics

District Gazelle

Sitting Member Honourable Jelta Wong

Total Population 150,000 plus

Five (5) Local Level Toma Vunadidir, Reimber Livuan, Central

Gazelle,

Government areas Inland Baining, Lassul Baining

Province East New Britain

Total DSIP funds for 2007- K58.05 Million

2016

Balance as at 31st August K10,627,255

20171 | Gazelle DSIP Performance Audit Report 2007-2016

2 | Gazelle DSIP Performance Audit Report 2007-2016

Telephone: 301 2203 Fax: 325 8295 Website: www.ago.gov.pg Email:

agopng@ago.gov.pgOFFICE OF THE AUDITOR-GENERAL

Honorable Job Pomat, MP

Speaker of the National Parliament

Parliament House

WAIGANI

National Capital DistrictDear Mr. Speaker

In accordance with the provisions of Section 214 of the National

Constitution of the -

Page 2 of 48

-

Independent State of Papua New Guinea, and the Audit Act 1989 (as

amended), I have

undertaken a Performance Audit on the District Services Improvement

Program

(DSIP).

I submit the report titled Gazelle District Services Improvement

Program (DSIP)

Performance Audit for years 2007-2016.

Following its presentation, receipt and tabling, the report will be

placed on the

Auditor-Generals Office of Papua New Guinea Homepage: www.ago.gov.pgMr. Gordon Kega, MBA, CPA

Acting Auditor-General

3 | Gazelle D S I P Performance Audit Report 2007-20164 | Gazelle D S I P Performance Audit Report 2007-2016

Contents

ACRONYMS AND DEFINITIONS

7

EXECUTIVE SUMMARY

8

INTRODUCTION

8

AUDIT OBJECTIVE, CRITERIA, SCOPE AND METHODOLOGY

8

AUDIT OBJECTIVE

8

CRITERIA

8

SCOPE

9

AUDIT METHODOLOGY

9

AUDIT CONCLUSION

9

RECOMMENDATIONS

12

RECOMMENDATION 1

12

RECOMMENDATION 2

12

RECOMMENDATION 3

13

RECOMMENDATION 4

13

RECOMMENDATION 5

14

CHAPTER 1. FINANCIAL ARRANGEMENTS

15 -

Page 3 of 48

-

CONCLUSION

15

KEY FINDINGS

15

CHAPTER 1 FINDINGS

16

FUNDING ALLOCATION FOR DSIP

16

TOTAL DSIP FUNDS DISBURSED TO GDDA FOR YEARS 2007-2016

16

DATA OF TOTAL FUNDS RECEIVED NOT KEPT AND RECONCILED.

17

UNAVAILABILITY OF RECORDS PERTAINING TO YEARS 2007-2012

17

DATA FOR 2013-2014 WAS PARTIALLY MAINTAINED

17

RECOMMENDATION 1

19

RESPONSE

19

CHAPTER 2 EXPENDITURE TREND

20

CONCLUSION

20

KEY FINDINGS .

20

CHAPTER 2 FINDINGS

21

RECOMMENDATION 2

23

RESPONSE

23

CHAPTER 3. EXPENDITURE NOT IN LINE WITH THE DSIP GUIDELINES

24

CONCLUSION

245 | Gazelle D S I P Performance Audit Report 2007-2016

KEY FINDINGS

24

CHAPTER 3 FINDINGS

25

TOKEN OF APPRECIATION PAYMENTS

25

GHOST NAMES PAID WAGES FROM GAZELLE DISTRICT TRUST OPERATING

ACCOUNT (DTOA) 26

GAZELLE DEVELOPMENT ROAD MANAGEMENT UNIT (GDRMU)

26

QUESTIONABLE PAYMENT TOTALLING K18,000 MADE TO AIM GLOBAL AS

SCHOOL FEE ASSISTANCE IN

2015

29 -

Page 4 of 48

-

RECOMMENDATIONS 3

29

RESPONSE

29

CHAPTER 4. PROCUREMENT OF INFRASTRUCTURE AND THE TENDERING PROCESS

30

CONCLUSION

30

KEY FINDINGS

30

CHAPTER 4 FINDINGS

31

EXAMPLES OF GDDA PROJECTS WITH POOR PROCUREMENT OF PROJECT

MANAGEMENT PRACTICES 32

INCOMPLETE KEREVAT MARKET AT THE COST OF K 3 MILLION

33

INCOMPLETE TOKIALA FIBRE GLASS PROJECT, COST OF K489,782.30 IN

2015 AND 2016 33

CONFLICT OF INTEREST IN THE TOKIALA FIBREGLASS PROJECT

34

KEREVAT RURAL HOSPITAL UNCOMPLETED X-RAY ROOM RENOVATION, COST OF

K121,588 38

PAYMENT TO AN INDIVIDUAL PERSON TOTALLING K30,000 IN 2014 FOR WORK

THAT WAS NOT VERIFIED BY

AUDIT.

39

RECOMMENDATION 4

39

RESPONSE

40

CHAPTER 5. MANAGEMENT OF FIXED ASSETS

41

CONCLUSION

41

KEY FINDINGS

41

CHAPTER 5 FINDINGS

41

ASSET MANAGEMENT

41

RECOMMENDATION 5

43

RESPONSE

43

APPENDIXES

44

LIST OF TABLES

44

LIST OF FIGURES

44 -

Page 5 of 48

-

6 | Gazelle DSIP Performance Audit Report 2 0 0 7 – 2 0 1 6

Acronyms and Definitions

Acronym Definition

CSTB Central Supply Tenders Board

DIRD Department of Implementation and Rural Development

DTOA District Treasury Operating Account

DSG District Support Grant

DSIP District Services Improvement Program

EDF Electoral Development Funds

ENB East New Britain

GDRMU Gazelle Development Road Management Unit

GDDA Gazelle District Development Authority

KRH Kerevat Rural Hospital

LEL Log Export Levy

LLG Local-level Government

PF(M)A Public Finance (Management) Act 1995

PFD Project Formulation Document

PGAS PNG Government Computerized Accounting System

PID Project Initiation Document

PSIP Provincial Services Improvement Program

PSTB Provincial Supply and Tender Board7 | Gazelle D S I P Performance Audit Report 2007-2016

Executive Summary

Introduction

Since the 1980s, the Government of PNG has allocated funding to

Members of

Parliament (MPs) to spend in their electorates known as the

Electoral Development

Fund (EDF). PNG has 89 open electorates (usually made up of one or

more districts).In 2007, the Government of PNG introduced the District Services

Improvement

Program (DSIP) program replacing the Electoral Development Fund

(EDF). Under the

DSIP, government funding of K10million was to be made available to

each District.The District Development Authority Board (previously known as the

Joint District

Planning Budget Priorities Committee (JDPBPC)) was the decision-

making body for -

Page 6 of 48

-

the DSIP and has ultimate responsibility on how the funds are spent.

It is chaired by

the MP of the district (or electorate) and also includes Local-Level

Government (LLG)

presidents and community members.The DSIP is not a discretionary account for MPs to use as they wish.

The Government

intends for the DSIP funds to finance basic infrastructure, and to

improve service

delivery. In 2013, the Department of Implementation and Rural

Development (DIRD)

issued administrative guidelines for spending DSIP funds. The

guidelines stated that

at least 40 per cent of this funding is to be spent on service

improvement in the areas

of health and education.Audit objective, criteria, scope and methodology

An independent audit of the Gazelle District Support Improvement

Program (DSIP)

was requested by the Member (MP) for Gazelle District, Honourable

Jelta Wong in

September 2017. The Auditor-General considered the request and

decided to

commence an audit on this matter.

Audit Objective

The objective of the audit was to examine and ascertain the

authenticity of the DSIP

expenditure payments in compliance with Government procurement

process, DSIP

procedural requirements and applicable legislation.

Criteria

To form a conclusion against this audit objective, the AGO examined

and ascertained

whether:

• DSIP expenditure payments complied with Government procurement

process,

procedural requirements and applicable laws (including DSIP

Guidelines,

Finance Instructions, Public Finance Management Act (1995 as

amended), and

the Legislations of Papua New Guinea).8 | Gazelle D S I P Performance Audit Report 2007-2016

• Management and acquittals including monitoring and reporting

requirements

were adhered to.

• Goods and services have been received for the funds expended and

value for

money was achieved. -

Page 7 of 48

-

Scope

Audit covered the Gazelle District Development Authority (GDDA) and

DSIP

programs and projects around the Gazelle District and looked into

the following areas:

• Payments and expenditures for the period 2013-2016 fiscal years

• Billing and Accounting Practice

• Corporate Governance

• Management Internal Controls and systems

• Asset Management

• Projects Inspection and Verification

• Management of Infrastructure Contracts

• Cash Book and Bank Reconciliations

• Human Resources

Audit Methodology

The audit team employed a number of data collection methods and

techniques

including:

• examination of expenditure records and source documents;

• data analysis and recalculations of payment amounts;

• project inspection and verification;

• the assessment of systems and payment process in place including

survey using

questionnaire;

• reviewing of DSIP key policy documents such as DSIP

Administrative

Guidelines and Finance Instructions, District Corporate plans,

PFMA 1995, and

relevant legislations; and

• interviewing key officers of the Gazelle District Development

Authority

(GDDA).Audit Conclusion

The Gazelle District Development Authority (GDDA) has not complied

with all

Government procurement process, DSIP procedural requirements and

applicable

legislation, regarding DSIP expenditure. The findings from this

audit are serious with

a number of suspicious and potentially fraudulent transactions

detected. The audit

inspections also revealed that a number of projects undertaken by

GDDA had either

nothing to show for the expenditure (a ‘ghost’ project), or were

left incomplete or

completed to a substandard level, despite the full project costs

being spent.9 | Gazelle D S I P Performance Audit Report 2007-2016

The GDDA did not maintain appropriate supporting documentation to

validate DSIP -

Page 8 of 48

-

expenditure. Examples of missing documentation included invoices,

payment

vouchers, contractual agreements, certificates of completion, tender

documents,

quotations, bank reconciliations, development plans, project

reports, fixed assets

registers and minutes of meetings.This gives rise to non-compliance with the requirements of the

Finance Instruction

and the Public Finances (Management) Act and increases the risk of

irregularities,

fraud and error with respect to the application of DSIP funds.It was also found that the District Treasury Operating Account

(DTOA) has been used

to receive other funding in addition to the DSIP funds. Utilising

the DTOA for other

deposits reduces the ability of the Government to hold Districts

accountable for the

manner in which DSIP funds are spent. Further, in a majority of

cases the difference

between the DSIP funds disbursed and deposited in the trust account

has not been

reconciled. Accordingly, it is not possible to accurately determine

where funds have

been received from and the intended purpose of the funds.The strategic planning framework has not been fully implemented

across the district

and was not operating as intended. Key documents, including the

Five-Year District

Development Plan, approved budgets and the prioritised list of

projects were not

followed. As a result, spending has not been well-directed, and

funds have been spent

on projects outside the aims of the DSIP.Actual expenditure from Gazelle District is not consistent with the

proportions

mandated and recommended by the DSIP program requirements. This

creates a risk

that some sectors will not receive the specified proportion of

funding and benefits of

the program will not be appropriately spread around the District.

The desired

outcomes of the DSIP are not being achieved and certain areas of

focus of the DSIP are

receiving little or no benefit.It was noted that a considerable amount of expenditure was

undertaken on items

outside the DSIP guidelines. On areas including: tokens of

appreciation; Wages; School -

Page 9 of 48

-

Fees Assistance; Gazelle District Road Management Unit (GDRMU); and

maintenance.There appear to be limited processes in place to manage and monitor

the progress of

projects or the performance on sub-contractors. Further, there is

limited use of signed

contracts to formalise the subcontracting relationship with service

providers. These

malpractices have resulted in value for money not being achieved by

the District.10 | Gazelle D S I P Performance Audit Report 2007-2016

Further, limited use of a competitive tender process increases the

risk of irregularities

and fraud.The impacts from the malpractices shows that, there are many

infrastructure projects

that have been fully paid for by GDDA but remain either incomplete

or completed to

a substandard level. Due to the limited use of contracts at a

District level there is

limited recourse against non-performing sub-contractors that have

been utilised.The GDDA’s management of assets is not effective. The fixed assets

register is

incomplete and not properly maintained. This was evident in the

audit tests results,

which found that a large number of assets could either not be

located or were identified

as damaged. The lack of maintaining and updating an asset register

creates the

potential of mismanagement and theft of GDDA assets. -

Page 10 of 48

-

11 | Gazelle D S I P Performance Audit Report 2007-2016

Recommendations

Recommendation 1

AGO recommends that the Gazelle District Development Authority

(GDDA):

1. Ensures that financial records and data for financial years 2012

back to prior

years are tracked and kept to ensure accountability of GoPNG DSIP

funds.

2. Builds proper and secure storage rooms for records management to

safeguard

the records of the GDDA.

3. Properly and accurately records all funds received, and

reconciles these to the

District Treasury Operating Account (DTOA) on a timely basis and

corresponds with the financial data that is sent by GDDA to

Department of

Finance Head Quarters in Port Moresby.

Gazelle District Development Authority Response: Agreed

Recommendation 2

AGO recommends that the Gazelle District Development Authority

(GGDA):

1. Complies with the funding guidelines of DSIP by sector and

implement the

sector programs accordingly to ensure that services are

delivered to the

population according to the government’s plan by sector.

2. Establishes a monitoring system to track expenditure by

program against

its DSIP expenditure in Gazelle District, so that it can clearly

track its level

of development against its development plan.

3. Replaces the five (5)-year development plan which lapsed at

the end of 2017

with a new multi-year development plan that will guide GDDA and

drive

developments. -

Page 11 of 48

-

Gazelle District Development Authority Response: Agreed

12 | Gazelle D S I P Performance Audit Report 2007-2016

Recommendation 3

AGO recommends that the Gazelle District Development Authority

(GGDA):

1. Immediately stop all expenditures out of the DSIP funds that

are not in line

with the funding arrangements. Appropriate disciplinary/legal

action is also

required against:

• Officers who abused their authority to pay themselves

excessive

“Tokens of Appreciations”;

• Officers responsible for using GDDA funds to pay salaries

for

individuals who are not employed by the district (termed

‘Ghost Names’

in this audit); and

• Officers that were responsible for making a payment of

K18,000 in the

disguise of School fee assistance to the pyramid scheme ‘Aim

Global’.

2. Should not use the District Support Grants (DSG) and DSIP funds

that come

into the District Treasury Operating Account (DTOA) to maintain

GDDA’s

business arm Gazelle District Road Management Unit (GDRMU). This

is in

breach of the DSIP guidelines.

3. Review the long term viability of maintaining the GDDA business

arm

GDRMU, and whether the benefits outweigh the costs of continuing

it.

Gazelle District Development Authority Response: Agreed

Recommendation 4

AGO recommends that the Gazelle District Development Authority -

Page 12 of 48

-

(GGDA):

1. Takes appropriate management action on the Contractors and

Officers tasked

to manage the projects listed below:

• Kerevat Market — non-existent despite spending K3 million;

• Tokiala Fibre Glass Project — non-existent despite spending

K489,782.30;

• Utmei Aidpost upgrade — unfinished despite spending K321,000;

• Vunapalading Construction of the Kerevat Health Centre Nurses

Duplex —

unfinished despite spending K320,000;

• Kerevat Rural Hospital X-ray Room Renovation — incomplete

despite

spending K151,588; and

• The maintenance invoice for work at Kerevat Rural Hospital

(KRH)

totalling K30,000 being paid to an individual, which the AGO

could not

verify.

2. Establishes controls on Procurement & Tendering to ensure

compliance with

the DSIP guidelines, PFMA and relevant legislations. This should

ensure that

project designs, costs, monitoring and reporting is done in a

manner consistent

with the allowable standards.

3. Reviews the quality and qualifications of officers that it

currently employs in

the administration. This review should be conducted in

consultation with the

Provincial Works Office. The GGDA should upskill current staff

or advertise13 | Gazelle D S I P Performance Audit Report 2007-2016

for skilled personnel that are efficient and effective in

delivering tasks and

programs.

Gazelle District Development Authority Response: Agreed

Recommendation 5

AGO recommends that the Gazelle District Development Authority

(GGDA):

1. Undertake a stocktake of all government assets, building, plant,

equipment

vehicles furniture’s and fittings, and a centralised asset

management system is

developed and maintained by a dedicated officer to ensure that

all assets are

accounted for.

2. Have a dialogue with the East New Britain (ENB) Provincial

Administration to

review the policy for disposing of vehicles after 3 years. This -

Page 13 of 48

-

is a costly exercise

and the GDDA has no budget for buying new vehicles or machinery

for the

DSIP sectoral programs.

Gazelle District Development Authority Response: Agreed14 | Gazelle D S I P Performance Audit Report 2007-2016

Chapter 1. Financial Arrangements

Conclusion

Gazelle DSIP did not maintain appropriate supporting documentation

to validate DSIP

expenditure. Examples of missing documentation included invoices,

payment vouchers,

contractual agreements, certificates of completion, tender

documents, quotations, bank

reconciliations, development plans, project reports, fixed asset

register and minutes of

meetings.This gives rise to non-compliance with the requirements of the

Financial Instructions

and the Public Finances (Management) Act and increases the risk of

irregularities, fraud,

and error with respect to application of DSIP funds. -

Page 14 of 48

-

It was also found that the District Treasury Operating Trust Account

(DTOA) has been

used to receive other funding in addition to the DSIP funds.

Further, in a majority of

cases the difference between the DSIP funds allocated and deposited

in the DTOA and

total funds received has not been reconciled. Accordingly, it is not

practical to accurately

determine where funds have been received for the intended purpose of

the funds.This has the effect of the district having access to additional

funding with no clear

direction as to how these funds should be spent. Further, utilising

the DTOA and DSIP

account for other deposits reduces the ability of the Government to

hold districts

accountable for the manner in which DSIP funds are applied.

Key Findings

A total of K58.05 million was disbursed as DSIP to the Gazelle

district for years 2008-

2016. The DSIP funding was managed under the account named “District

Treasury

Operating Trust Account”. This account held all other funds for the

district, including:

• District Support Grants (DSG);

• National Agriculture Development Program (NADP); and

• Log Export Levy (LEL).Audit review of the financial management of GDDA found that no

record has been kept to

account for all the funds received into the district despite having

a full finance team

(Treasurer, Accountant and 2 accounts clerk’s/officers) stationed at

the District Treasury

Office.The Audit found that records and back-up data were not retained from

2007-2012. The

risk and impact it poses on management is very high on areas such

as:

•Accountability of expenditures undertaken over the last 10 years;

•Location of assets that were purchased over the last 10 years that

are not included in

the asset register;

•Document trail accounting, auditing and management purposes; and

•Accuracy of acquitted reports submitted to the Department of

Infrastructure and Rural

Development (DIRD) and Department of Finance.Management file documentation was very poor, including that:

15 | Gazelle DSIP Performance Audit Report 2007-2016

-

Page 15 of 48

-

• The files were stacked outside the treasury office accessible to

the public;

• No filing cabinet exists;

• Minutes of meetings were not properly filed;

• Contract files were not maintained; and

• Personnel files were poorly managed.Chapter 1 Findings

Funding allocation for DSIP

The National Executive Council (NEC) Decision NG 414/2013

decision made on

18th November 2013, and subsequent Finance Instructions 2/2014

& Finance

Instruction 1 of 2015 directed for District Support

Improvement Program and

funding on sectoral basis. These key sectors are shown in

Table 1.

Table 1: Distribution of DSIP K10 million through sectors 2013-2016Sector Funding K10million total

Allocation

Infrastructure 30% K3million

Health 20% K2million

Education 20% K2million

Law and Justice 10% K1million

Economic & Agriculture 10% K1million

Administration 10% K1million

(K300,000 General Admin (30%))

(K300,000 MP Office Support

(30%))

(K400,000 Project Mobilisation

(40%))

Source: DSIP Administrative Guidelines 1B/2014 (1st January 2014).Total DSIP funds disbursed to GDDA for years 2007-2016

Table 2: Total DSIP Funds allocated and Released to Gazelle District

2007 2008 2009 2010 2011 2012 2013 2014 2015

2016DSIP GDDA Not Available4m 6m 5m 3m 2m 10m 10m 8.05m

10m

Total K58,050,000 (K58.05million)1

Note 1: The K58.05 million is only the DSIP component for years

2008-2016, all the other

grants that go into this account is not factored in this

total.

Source: Department of Implementation and Rural Development audited

report.

While the Gazelle district was notionally allocated K10

million per year, for a

total of K90 million from 2008-2016. According to the Table 2, -

Page 16 of 48

-

a total of

K58.05 million was disbursed to Gazelle district as DSIP for

that period, from

the Department of Implementation and Rural Development

records. The

GDDA does not maintain any data or documentations to show that

they

received these funds.16 | Gazelle DSIP Performance Audit Report 2007-2016

Bank Accounts

Part 6.1 of the Department of Finance, Financial Instructions 1

of 2015

regarding the functional arrangement for the District

Development Authority

(DDA), states that the:

District Development Authority will utilise the existing

District/Provincial

Treasury operating Account to make expenditure, payments

and do receipting

of DSIP funds until as and when need arises to establish

another trust account

then a formal request must be made to Secretary of Finance

providing full

explanations.

The DSIP funds in Gazelle is managed under the account named

“District

Treasury Operating Account” (DTOA) with the Bank of South

Pacific. The same

account holds the districts other funds, including the:

• District Support Grants (DSG);

• National Agriculture Development Program (NADP); and

• Log Export Levy (LEL).

Data of Total Funds received not kept and reconciled.

Audit review of the financial management of GDDA found that no

records or

ledgers were maintained to account for all the funds received.

The GDDA undertook no reconciliation of dispersed DSIP

allocations with

actual funds received by the District. Accordingly, the audit

was unable to verify

that the budgeted DSIP allocations have been disbursed across

the District as

intended.

Control weaknesses over recording of revenue can lead to fraud

and poses a

high risk of inaccurate accounting of revenue records.

Unavailability of records pertaining to years 2007-2012

Audit review of the systems and controls surrounding the

receipting and

collection of revenues were noted to be weak and needed

addressing. Including -

Page 17 of 48

-

that the revenue data pertaining to years 2007-2012 could not

be confirmed by

AGO, due to poor records management at the GDDA.

The GGDA confirmed that no data pertaining to years 2007-2012

was kept at

the Gazelle District. Without this financial data the district

could not monitor

and take stock of the assets and projects that were carried out

in the district.

Data for 2013-2014 was partially maintained

• Data for 2013-2014 was partially maintained but soft/hard

copies of the Papua

New Guinea Accounting System (PGAS) could not be obtained due

to

unavailability of PGAS Server at the District.

• AGO was advised that East New Britain was one of the Provinces

where the

Governments new Integrated Financial Management System (IFMS)

was rolled

out and all PGAS servers were replaced with the IFMS in 2016.17 | Gazelle D S I P Performance Audit Report 2007-2016

Without access to the records or back-up data, there is a very

high risk and

impact on areas such as:

• Accountability of expenditures undertaken over the last 10

years;

• Location of assets that were purchased over the last 10 years

that are not

included in the asset register;

• Document trail accounting, auditing and management purposes;

and

• Accuracy of acquitted reports submitted to DIRD and Department

of Finance.District Treasurer failed to allow AGO officers access to GDDA

records

Despite the District Treasurer confirming and signing the Local

Audit Query

(LAQ) that no data was backed up and kept in the district,

further audit inquiry

with the District Accountant confirmed that they did maintain

copies of the data

for 2015 and 2016. This data was then made available to the

audit team.

The attempt to keep government records from Auditor-Generals

Office is a

breach of section 213 & 214 of the National Constitution on the

powers of the

Auditor General.Document Management

-

Page 18 of 48

-

For accurate accounting and financial purposes, the Public

Finance

Management Act (PFMA) requires that financial data and

information must be

kept to account and record all transactions of the District

Accounts. The PFMA

also requires that all financial documents be maintained in a

proper and secure

storage area, to establish financial trails to expenditures

which can be used by

other financial entities as well a management to track

expenses.

Figure 1: Gazelle District Development Authority (GDDA) Financial

Records stacked outside the

GDDA treasury officeGDDA was found to have poor controls regarding the management

of financial

records management, as shown in Figure 1. These files were

stacked outside the

treasury office which were easily accessible to the public. AGO

found that there

was:18 | Gazelle D S I P Performance Audit Report 2007-2016

• No filing cabinet to properly store the financial documents of

the district;

• No documents pertaining to years 2007-2009 were kept;

• Minutes of Meetings were not properly filed, they should be

filed and kept in

the administrator’s office;

• Contract files were not kept; and

• Personnel files were poorly managed.Recommendation 1

AGO recommends that the Gazelle District Development Authority -

Page 19 of 48

-

(GDDA):

1. Ensures that financial records and data for financial years

2012 back to prior

years are tracked and kept to ensure accountability of GoPNG

DSIP funds.

2. Builds proper and secure storage rooms for records management

to safeguard

the records of the GDDA.

3. Properly and accurately records all funds received, and

reconciles these to the

District Treasury Operating Account (DTOA) on a timely basis

and

corresponds with the financial data that is sent by GDDA to

Department of

Finance Head Quarters in Port Moresby.

Response

Gazelle District Development Authority agreed with findings.19 | Gazelle D S I P Performance Audit Report 2007-2016

Chapter 2 Expenditure trend

Conclusion

The strategic planning framework has not been fully implemented

across the district and

was not operating as intended.Key documents, including the Five-Year District Development Plan,

approved budgets -

Page 20 of 48

-

and expenditure on sector programs not followed.

GDDA actual expenditure for years 2007-2016 did not follow the DSIP

program

guidelines. This resulted in sectors programs not receiving expected

funding proportions,

meaning that the intended benefits of the DSIP program was not

appropriately spread

around the District.

Key Findings .

Only data for 2013 to 2016 totalling K38.05million was tested due to

the lack of available

data and records for years 2007-2012.From the audited funds of K38.05million, only K20.1 million was

spend on the DSIP

required sectors.AGO notes that K17.95 Million from the 2013-2016 DSIP grants

released is un-accounted

for (equivalent to 47 per cent of released funds).While K10million was released in most years from 2013 to 2016, total

expenditure per

sector was below 50% for 2013 and 2014. As a result, most of the

programs for 2013 and

2014 were rolled over into years 2015 and 2016. The district has

been mainly

implementing rollover programs in recent years.20 | Gazelle DSIP Performance Audit Report 2007-2016

-

Page 21 of 48

-

Chapter 2 Findings

2.1 Only data for 2013 to 2016 totalling K38.05million was

tested due to the lack

of available data and records for years 2007-2012.

2.2 The audit noted that only K20.1 million was spent on DSIP

approved sectors

for the years 2013-2016 as shown in Figure 2.

2.3 Of the K38.05 million that DIRD has reported providing to

GDDA from 2013-

2016, a sum of K17.95 million is un-accounted for (equivalent

to 47 per cent of

received funds).

Figure 2: DSIP revenue vs Expenditure in Gazelle District from 2013

to 2016.

12,000,000

10,000,000

8,000,000

6,000,000

4,000,000

2,000,000

0 2013 2014 2015

2016

Amount Allocated Expenditure Rollover ExpenditureGraph Narrative

2.4 Figure 2 shows that despite government releasing K10million

to GDDA for

three of the four years from 2013-2016, total expenditure was

below 50% for

2013 and 2014. As a result, most of the programs for 2013 and

2014 were rolled

over into years 2015 and 2016. The district has been mainly

implementing

rollover programs in recent years.

2.5 The DSIP funding guidelines (discussed in Chapter 1) state

that the proportion

of DSIP expenditure for each sector should be:

• 30 per cent Infrastructure;

• 20 per cent Health;

• 20 per cent Education;

• 10 per cent Law and Justice;

• 10 per cent Economic & Agriculture; and

• 10 per cent Administration.21 | Gazelle D S I P Performance Audit Report 2007-2016

Figure 3: DSIP Expenditure by sector in Gazelle District for years

2013-2016

2.6 Audit analysis of the expenditure against sector programs in

Figure 3 found -

Page 22 of 48

-

that GDDA did not fully roll out the its 5 year plan because the

expenditures

on all sectors in the 4 years were below the 50% mark for all

sectors. The only

increased expenditure over the 5-year period was on infrastructure

(K4million

in 2016). This figure (K4million) was higher than the threshold for

one year

(K2million) and was confirmed with GDDA that the additional,

increase in

Infrastructure spending in 2015 and 2016 was due to:

o Outstanding invoices on projects for prior years expenditure being

carried forward covering years 2011-2014. Audit noted that most of

the

payments were based on minutes and resolutions from GDDA board

from 2011-2014.

Five (5)-year Plan for 2012-2017 was not fully implemented.

2.7 Audit is of the view that the 5-year Plan for GDDA covering

2012-2017 was not

fully implemented as the expenditure analysis shows that all the

goals of the

plan were not fully achieved.

2.8 The GDDA five (5)-year development plan lapsed at the end of

2017 and should

be replaced with a new multi-year development plan that will guide

GDDA and

drive developments.

22 | Gazelle D S I P Performance Audit Report 2 0 0 7 – 2 0 1 6

5,000,000

4,000,000

3,000,000

2,000,000

1,000,000

0

Economic

Health

Infrastructure

Community

Development

Law & Order

Education

Administration

2013

2014 2015

2016Recommendation 2

AGO recommends that the Gazelle District Development Authority

(GGDA):

1. Complies with the funding guidelines of DSIP by sector and

implement the

sector programs accordingly to ensure that services are

delivered to the -

Page 23 of 48

-

population according to the government’s plan by sector.

2. Establishes a monitoring system to track expenditure by

program against

its DSIP expenditure in Gazelle District, so that it can clearly

track its level

of development against its development plan.

3. Replaces the five (5)-year development plan which lapsed at

the end of 2017

with a new multi-year development plan that will guide GDDA and

drive

developments.

Response

Gazelle District Development Authority agreed with findings.23 | Gazelle D S I P Performance Audit Report 2007-2016

Chapter 3. Expenditure not in line with the DSIP Guidelines

Conclusion

DSIP funds are intended to be spent on the sectors identified in the

DSIP guidelines.

However, it was noted that a considerable amount of DSIP funds was

expended on items

outside the DSIP guidelines such as: Token of appreciation; Wages;

School Fees

Assistance; and sustaining its business arm, the Gazelle District -

Page 24 of 48

-

Road Management Unit

(GDRMU).AGO further concludes that, due to the costs associated with

maintaining a business arm

without a funding source, it is advisable that management review its

decision to maintain

GDRMU and whether the benefits outweigh the costs.The District Support Grants (DSG) and DSIP funds that come into the

DTOA should not be

used to maintain GDRMU. This is a breach of the financial

guidelines, which states what

DSG and DSIP funds can be used for.

Key Findings

Audit review uncovered that the Officers were paying themselves

cash/cheque payments

known as ‘token of appreciation’ for working overtime and/or other

reasons only known

to them. In 2015 and 2016, the audit found that a total of K125,989

was paid as token of

appreciation to the GDDA officers, and mostly to senior public

servants.Audit review of expenditures incurred by GDDA in 2015 and 2016 found

that a

substantial amount of administration funds (totalling K200,813) was

used to pay the

wages of casual staff. AGO further noted that, thirteen (13) casual

staff currently engaged

by GDDA, had been casual employees for more than three (3) years,

exceeding the six (6)

month allowable probation period.It was also uncovered that two ‘Ghost’ employees were being paid

wages from the District

Treasury Operating Account (DTOA).Proper planning and cost benefit analysis were not done to assess

whether GDDA had the

capacity to sustain the Gazelle District Road Management Unit

(GDRMU) which is a

Business arm of GDDA. A considerable amount of GDDA DSIP funds had

been used to

sustain, as well as maintain, GDRMU and its machineries. The GDDA

could not provide the

total revenue that was received for GDRMU for years 2007 to 2012.The GDRMU’s current practices of leasing machinery to construction

contractors poses a

very high risk of collusion. The GDDA officers and contractors could

defraud the State

through this arrangement, whereby the State is paying for the hire

of machinery that it -

Page 25 of 48

-

already owns.

A total of K1.3 million was paid as school fees assistance from the

DSIP funds between

2015 and 2016. The guidelines for DSIP clearly states that it is a

“service” improvement

program and not a grant to individuals.24 | Gazelle DSIP Performance Audit Report 2007-2016

The audit also found a fraudulent payment totalling K18,000 made to

AIM GLOBAL

Networking Pyramid Money scheme in the disguise of school fee

assistance.Chapter 3 Findings

Token of appreciation payments

3.1 Audit review uncovered that a number of mostly senior permanent

public

servants were paying themselves cash/cheque payments known as

‘token of

appreciation’ for working overtime and/or other reasons known

only to them.

For the 2015 and 2016 period, the audit found that a total of

K125, 989 were paid

as token of appreciation to the officers.

3.2 These officers are already paid a fixed salary to carry out

official government

duties. Receiving such a token is seen as Double Dipping. This is

an abuse of

public funds allocated for projects and the running of the

Administration, which

is in breach of Public Financial Management Laws and Public

Service General

Orders.

Table 3: Summary of payments made as token of appreciation for years

2015 & 2016Year AMOUNT

2015 39,948.00

2016 86,041.00

TOTAL 125,989.00

3.3 The audit further found that tokens of appreciation totalling

K24,200 were

suspiciously made on the 31st of December in both 2015 and 2016,

after the

annual close of accounts and shut down of government offices.

3.4 These payments are in breach of the DSIP guidelines as well as -

Page 26 of 48

-

the general

orders on the payment of allowances.

3.5 The District Treasury Operating Account (DTOA) should not allow

for irregular

payments that are not in line with the policies and legislations

of the

government. Nor should officers with financial position of trust

abuse their

positions to operate systems outside of the normal guidelines and

legislations.

3.6 In 2015 and 2016, the audit found that a substantial amount of

the

administration and internal revenue funds component (totalling

K200,814) was

used to pay the wages of casual staff.25 | Gazelle DSIP Performance Audit Report 2007-2016

Payment of Salaries and wages out of the DSG and DSIP accounts

Table 4: Total Wages paid from the District Treasury Operating

AccountYear Number of Total

payments2015 111 K76,380.84

2016 222 K124,433.00

Total 333 K200,813.80

3.7 According to the Human Resource Staff Establishment Register

obtained, there

were 13 casual staff working with the District at the time of the

audit. All

13 casuals had been working (as casuals) for more than 3 years,

exceeding the

6 months’ probation period. The long-term casual staff should

have been made

permanent by now (depending on the need of the job they are

doing) or laid off

to cut administration cost on staff wages. -

Page 27 of 48

-

Ghost Names paid wages from Gazelle District Trust Operating Account

(DTOA)3.8 The audit also found that three (3) payments totalling K900 were

paid in 2016

to two (2) individuals whose names were not on the Human Resource

Staff

Establishment Register. Such individuals are referred to as

‘ghost’ names.Gazelle Development Road Management Unit (GDRMU)

Problems with sustainability

3.9 GDRMU was formed back in 2007 as a business arm of the GDDA,

when heavy

machinery plant and vehicles were acquired to be used to develop

Gazelle

district. The audit found that proper planning and cost benefit

analysis were not

done to assess whether GDDA had the capability to sustain this

business idea

over the long term.3.10 Audit uncovered that from 2008 to 2012 GDRMU started facing

management

problems with maintenance of the machines and payment of GDRMU

staff.

Audit found that GDDA DSIP funds were being used to sustain as

well as

maintain GDRMU and its machinery.3.11 GDRMU did not have a funding source and was solely depended on

the GDDA

Treasury Account which holds DSG and DSIP funds to pay for:• the wages for GDRMU staff;

• maintenance of the fleet; and

• fuel for operations.26 | Gazelle D S I P Performance Audit Report 2007-2016

Inconsistencies in the Billing and Receipting for GDRMU raises

concerns of fraud

taking place. -

Page 28 of 48

-

3.12 The GDDA could not provide the total revenue that was received

for GDRMU

for years 2007 to 2012. It was also noted that invoices for the

usage of GDRMU

machinery were being raised by contractors and were cleared for

payments. This

practice poses a high risk of fraud because GDDA should not be

paying

contractors for machinery that they already own. Without a clear

receipting

system in place, the risk of theft and fraud is very high.

3.13 The current practice is that machinery is leased out to

construction contractors

who in turn raise the invoice inclusive of GDRMU leased machinery

back to the

DTOA for payment. This practice of leasing out and invoicing

GDRMU

machines poses a very high risk of collusion between GDDA

officers and

contractors to defraud the State, whereby the State is paying for

the hire of

machinery that they already own.

3.14 GDRMU are currently operating the following machinery that were

inspected

by audit:

• 1x Loader;

• 1x Roller;

• 1x Backhoe loader; and

• 1x Hino Earth Moving Truck.

3.15 Audit also found that there were no clear invoicing and

receipting process for

the hire of equipment, and individuals managing them fail to

produce revenue

listing or ledgers for machinery hire. Audit is concerned that

the risk of misuse

of GDDA assets benefiting a few individuals, has been found here

to be high

and urgently in need of addressing.

3.16 It was also noted that some machinery has now been grounded due

to special

maintenance needs and parts that can only be sourced from

specialist and

expensive companies. -

Page 29 of 48

-

27 | Gazelle D S I P Performance Audit Report 2007-2016

Figure 4: Some of the GDRMU machinery that needs maintenance and

replacement.3.17 The malpractices in the District has denied the much-needed

services and

infrastructure to the district. GDDA should ensure that these

findings are taken

seriously and address them.

3.18 It should also be noted that public officers and contractors

dealing in corruption

can be imprisoned up to seven years as specified under sections

61, 62, 87 and

9B of the Criminal Code 1974.

School Fee’s Assistance

3.19 A total of K1.3 million was paid as school fee’s assistance

from the DSIP funds

between 2015 and 2016.

Table 5: Total Paid as school fee’s assistance for years 2015 & 2016

Year School fee’s

assistance from DSIP

2015 K1,118,813

2016 K 162,200

Total K1,281,0133.20 The guidelines for DSIP clearly states that it is a “service”

improvement

program and not a grant to individuals. So, any expenditure on

school fees is

outside the DSIP guidelines. -

Page 30 of 48

-

28 | Gazelle D S I P Performance Audit Report 2007-2016

Questionable payment totalling K18,000 made to AIM GLOBAL as school

fee

assistance in 2015

3.21 Audit confirmed that there are no schools in Papua New Guinea

called Aim

Global and therefore concluded the K18,000 payment for ‘school

fee assistance’

in July 2015 is suspicious of being a fraudulent activity. A

fraud where the

officers intentionally made a dubious payment to the money

pyramid scheme

Aim Global in the disguise of school fee assistance.

3.22 Appropriate action should be taken against the Education

Coordinator and all

officers charged with overseeing school fees with regards to the

suspicious

payment.Recommendations 3

AGO recommends that the Gazelle District Development Authority

(GGDA):

1. Immediately stop all expenditures out of the DSIP funds that are

not in line

with the funding arrangements. Appropriate disciplinary/legal

action is also

required against:

• Officers who abused their authority to pay themselves

excessive

“Tokens of Appreciations”;

• Officers responsible for using GDDA funds to pay salaries for

individuals who are not employed by the district (termed

‘Ghost Names’

in this audit); and

• Officers that were responsible for making a payment of K18,000

in the

disguise of School fee assistance to the pyramid scheme ‘Aim

Global’.

2. Should not use the District Support Grants (DSG) and DSIP funds

that come

into the District Treasury Operating Account (DTOA) to maintain

GDDA’s

business arm Gazelle District Road Management Unit (GDRMU). This

is in

breach of the DSIP guidelines.

3. Review the long term viability of maintaining the GDDA business

arm

GDRMU, and whether the benefits outweigh the costs of continuing

it.

Response

Gazelle District Development Authority agreed with findings. -

Page 31 of 48

-

29 | Gazelle D S I P Performance Audit Report 2007-2016

Chapter 4. Procurement of Infrastructure and the tendering process

ConclusionAudit observed that the District did not have qualified engineer/

personnel to review

infrastructure designs, or to ensure that projects, costs, designs,

and monitoring was done

in a manner consistent with the allowable standards.The Finance Instruction establishes procedures for the screening,

selection and approval

of service providers. Gazelle District has performed very poorly

against these

requirements due to lack of quotations, ineffective tender

processes, poor selection of

preferred suppliers/contractors, splitting of project costs to

circumvent the procurement

requirements and proper approvals/authorisation not being obtained.There appear to be limited processes in place to manage and monitor

the progress of

projects, or the performance on sub-contractors. There is limited

use of signed contracts

to formalise the sub-contracting relationship with service

providers.The poor controls surrounding procurements of infrastructure and the

tendering

processes has increased the risk that value for money is not being

achieved by the GDDA,

due to competitive tender processes not taking place. Further,

limited use of a

competitive tender process increases the risk of irregularities and

fraud. This was evident

in the number of uncompleted projects, and ghost project that were

uncovered during

the audit that are highlighted in the key findings

Key Findings

Audit noted weaknesses in the procurement controls at the GDDA

including payments -

Page 32 of 48

-

being split in order to work around the procurement requirements of

the Public Finances

(Management) Act and the Finance Instruction.Further, the process of requesting quotations is non-existent and

the authorisation of

purchase orders is limited. This results in:

• Bypassing of government procurement process;

• Over-inflated costs;

• Rollover projects;

• Incomplete projects; and

• Non-Existent projects.Audit noted that Gazelle District Development Authority did not have

qualified

engineer/personnel to review infrastructure designs, or to ensure

that projects, costs,

designs and monitoring was done in a manner consistent with the

allowable standards.The Project Initiation and Formulation Documents (PID/PFD) are

poorly designed and

documented without proper scrutiny and assessment by qualified

technical engineers to

give a realistic cost of the project before the awarding of

contracts. As a result of poor

project documentation and engineering scoping design in the initial

stage of project30 | Gazelle DSIP Performance Audit Report 2007-2016

planning, most projects funded were not completed on time, were

carried over to

following year and/or remained outstanding.The audit uncovered a “ghost project” whereby K3million was spent to

build a market in

Kerevat, but to date there is nothing but an empty plot of land at

the site of the proposed

Kerevat Market.The audit also found that K489,782 had been spent on another “ghost

project” Tokiala

Fibre Glass Project during 2015-2016. The audit confirmed through

site inspection that

this project does not exist, except for a fenced area and a small

makeshift office.The audit is concerned that there was a conflict of interest between

the Chairman of the

GDDA and the company that was engaged to build the Tokiala Fibre

Glass Project. The

GDDA Chairman was a director of the company when it registered with -

Page 33 of 48

-

IPA on the 2nd of

February 2015, and the audit found that directives were issued by

the chairman to pay

for invoices that related to this project for years 2015-2016.Audit inspections revealed that a number of projects under taken by

GDDA were left

incomplete despite being paid the full project funds. Most of these

projects were

undertaken by the same suppliers and have been rolled over from the

previous years.Chapter 4 Findings

Procurement processes in the DDA guidelines as well as Public

Finance

Management Act and Finance Instruction 1 of 2015 not adhered to.

The audit observed that the District did not have qualified

engineer/personnel

to review infrastructure designs, or to ensure that projects,

costs, designs and

monitoring was done in a manner consistent with the allowable

standards.

The audit found that the Project Initiation and Formulation

Documents

(PID/PFD) were poorly documented without proper scrutiny and

assessment by

qualified technical engineers to give a realistic cost of the

project before the

awarding of the contract. This has resulted in high additional

inflated cost

and/or variation cost to the projects and the completed projects

does not reflect

the real value of money spent. As a result of poor project

documentation and

engineering scoping design in the initial stage of project

planning, most funded

projects were not completed on time, and were carried over to

following year

and/or remained outstanding.

Use of Third Party for tendering out GDDA projects

The audit found that the GDDA contracts out some of the major

Infrastructure

projects to the Gazelle Restoration Authority (GRA). The GRA is

not a

construction company, but a consultancy entity of the East New

Britain

Province.

Payments under this arrangement are a waste, as the funding for

the program

is spent on consultancy fees instead of the intended project.31 | Gazelle DSIP Performance Audit Report 2007-2016

-

Page 34 of 48

-

Less than 300 meters of the road sealed for K1.8 Million

An example of a GDDA project to include the GRA as a middleman,

is the

VURAVURAI Road Project. This project used K1.8million (almost 98%

of

Infrastructure allocation) for re-resealing 300 metres of an

existing road at

Vuravurai.

Under this arrangements all tender and contract documents for

this road

project was managed by GRA. GRA’s consultancy fees for the

K1.8million

project totalled K500,000 (almost 28% of the project funding).

Figure 5: Vuvurai Road less than 300meters resealed for K1.8 millionExamples of GDDA projects with poor procurement of project

management

practices

The audit found a number of examples of poor procurement or

project

management practices in Gazelle District, including:

Kerevat Market;

Tokiala Fibre Glass Project;

Utmei Aidpost upgrade;

Vunapalading Construction of the Kerevat Health Centre Nurses

Duplex;

Kerevat Rural Hospital X-ray Room Renovation; and

Maintenance work at Kerevat Rural Hospital.32 | Gazelle D S I P Performance Audit Report 2007-2016

-

Page 35 of 48

-

Incomplete Kerevat Market at the Cost of K 3 million

Key Findings for this project:

• No Contract or Project Initiation Document;

• Over inflated cost;

• Tendering document not found (above K500,000); and

• No Progressive work reports to justify payments.

Despite paying K3milion for the construction of the Kerevat

Market, there is

nothing to show for that expenditure, see Figure 6.

Figure 6: Image of the empty space taken in November 2017 where the

proposed K3Million

Kerevat Market was to have been built.All officers that were involved in the project should be held

accountable and

investigated for possible intentions to commit fraud.

Incomplete Tokiala Fibre Glass Project, cost of K489,782.30 in 2015

and 2016

Key Findings for this project:

• No Contract or Project Initiation Document;

• Over Inflated Cost;

• Tendering Document not found (above K500,000); and

• No Progressive work reports to justify payments.33 | Gazelle D S I P Performance Audit Report 2007-2016

Despite payment of K489,782.30 for years 2015 and 2016, the audit

inspection -

Page 36 of 48

-

of the site revealed that the amount of work done does not

reflect the amount

of money spent.

Figure 7: Image shows the empty space and the fencing for Tokiala

Fibre Glass, taken in

November 2017Conflict of interest in the Tokiala Fibreglass Project

Company search shows that the former Chairman of GDDA was a

director of

the company when it registered with IPA on the 2nd of February

2015 and had

shares in the contractor engaged to deliver this project.

Review of the payment documents found that directives were issued

by the

former chairman of GDDA to pay for invoices that related to this

project which

totalled to K489,782 despite not having any project monitoring or

progress

reports to justify them being paid.

The subsequent payments from the District need to be investigated

for fraud

because the inspection exercise that was carried out by the audit

on the 8th of

November 2017 found that there was nothing in the proposed site

for the Fibre

Glass Project to justify for the amounts of funds that was

released on the

directive of the Former Chairman.

Audit found that there were no progressive work reports to

justify the amount

of funds that were released for this project. -

Page 37 of 48

-

34 | Gazelle D S I P Performance Audit Report 2007-2016

Utmei Aidpost Upgrade, cost of K321,000

Key findings for this project:

• People with no access to health services due to incomplete

project;

• No Contract;

• No Project initiation Document;

• Resource Wastage;

• Over Inflated Cost;

• Tendering Document not found; and

• No Progressive work reports to justify payments.

Figure 8: Utmei Aidpost left unfinished and unoccupied due to

incomplete infrastructure

and bad planning. -

Page 38 of 48

-

35 | Gazelle D S I P Performance Audit Report 2007-2016

Prior to AGO inspections, the building was listed as 100%

complete from the

list obtained from the infrastructure program officer. Audit

inspection found

the building was incomplete and was covered with overgrown brush.

Construction of Duplex Building for Kerevat Hospital On-call Nurses

at

Vunapalading, cost of K320,000

Located 30 minutes’ drive away from the Kerevat Rural Hospital

this facility

was supposed to have been used for on call nurses.

Key findings for this project:

• No Contract;

• No Project initiation Document;

• Resource Wastage;

• Over Inflated Cost; and

• No Progressive work reports to justify payments.

GDDA paid the construction company the full cost of K320,000 and

listed the

house as completed in the infrastructure listing. The audit

inspection found that

the house was incomplete, with no water connections and no

electricity. The

audit inspection of the property noted that the wood used to

construct the

property was starting to show signs of termite infestation and

the building was

starting to rot away. This was despite it being a new building

that was not yet

occupied.

The Contractor should be held accountable for the gross wastage

of GDDA

funds and made to complete the building with its own funds or

appropriate

action taken on future business engagements with the supplier. -

Page 39 of 48

-

36 | Gazelle D S I P Performance Audit Report 2007-2016

Figure 9: Vunapalading Uncomplete Construction of the Kerevat Health

Hospital Oncall

Nurses DuplexFloor Rotting as

well as the stair

casingAGO noted that the same contractors have been given new projects

at the time

of audit despite failing to complete infrastructure projects at

Utmei Aidpost

Upgrade and Vunapalading Duplex Building.

The GDDA have shown gross negligence of their roles and

responsibilities to

ensure that much needed services and infrastructure is provided

to the people

of the Gazelle district.

Need for an on-call hostel for Nurses at Kerevat Rural Hospital

With the on-call Nurses accommodation described above being

unfinished,

personnel at Kerevat Rural Hospital advised the audit that On

Call Nurses did -

Page 40 of 48

-

not have a place to stay when on duty. A Storage Room was used by

nurses as

the temporary live in quarters, which is cramped.37 | Gazelle D S I P Performance Audit Report 2007-2016

Figure 10: Current Facility used by on call nurses at Kerevat Rural

Hospital. A makeshift

store-room converted to sleeping room.The audit also found that there was enough land inside the

Kerevat Rural

Hospital premises to build an on call hostel for the nurses and

medical officers.

This would appear to be a more sensible option than a facility

that is located 5

kilometres away from the Hospital.

Kerevat Rural Hospital Uncompleted X-ray Room Renovation, cost of

K121,588

Key Findings for the project:

• Incomplete;

• Over Inflated Cost;

• Wastage of resource;

• No progressive reports to justify payment; and

• Breach of normal procurement processes to engage contractor. -

Page 41 of 48

-

Audit found that the X-ray room was incomplete and also the

equipment that

was bought for the X-ray room was still sitting idle in the

District Health Sector

Program Officer’s office.

Procurement Requirements and the health standard design

requirements for an

X-ray room were not followed to construct this vital part of the

Kerevat Rural

Hospital. The construction was also undertaken by an individual

which is a

breach of the Finance Management Act and the DSIP guidelines.38 | Gazelle D S I P Performance Audit Report 2007-2016

Figure 11:Image of the incomplete X-ray room

Payment to an individual person totalling K30,000 in 2014 for work

that was not

verified by audit.

Audit inspection of the Rural Hospital could not verify and

confirm the work

that was done by the individual that was paid K30,000 on 24

December 2014 for

maintenance services at the Kerevat Rural Hospital. The GDDA also

did not

provide any details as to the work done, why an individual was

engaged, or who

requested and approved this work.

GDDA should seriously take into consideration the quality and

qualifications of

officers that it currently employs in the administration and up

skill them or

advertise for skilled personnel that are efficient and effective

in delivering tasks -

Page 42 of 48

-

and programs.

Officers Responsible should be held accountable for the

incomplete projects as

they initiate the project identification, project scoping and

monitor and report

project results.

Audit recommends that management adhere to the Governments set

rules,

procedures and regulations as per the Finance Instructions, ORD

Administrative Guidelines and PFMA in awarding contracts to the

contractors.Recommendation 4

AGO recommends that the Gazelle District Development Authority

(GGDA):

1. Takes appropriate management action on the Contractors and

Officers tasked

to manage the projects listed below:

• Kerevat Market — non-existent despite spending K3 million;

• Tokiala Fibre Glass Project — non-existent despite spending

K489,782.30;

• Utmei Aidpost upgrade — unfinished despite spending K321,000;39 | Gazelle D S I P Performance Audit Report 2007-2016

• Vunapalading Construction of the Kerevat Health Centre Nurses

Duplex —

unfinished despite spending K320,000;

• Kerevat Rural Hospital X-ray Room Renovation — incomplete

despite

spending K151,588; and

• The maintenance invoice for work at Kerevat Rural Hospital

(KRH)

totalling K30,000 being paid to an individual, which the AGO

could not

verify.

2. Establishes controls on Procurement & Tendering to ensure

compliance with

the DSIP guidelines, PFMA and relevant legislations. This should

ensure that

project designs, costs, monitoring and reporting is done in a

manner consistent

with the allowable standards.

3. Reviews the quality and qualifications of officers that it

currently employs in

the administration. This review should be conducted in

consultation with the

Provincial Works Office. The GGDA should upskill current staff or

advertise

for skilled personnel that are efficient and effective in

delivering tasks and

programs.

Response -

Page 43 of 48

-

Gazelle District Development Authority agreed with findings.

40 | Gazelle D S I P Performance Audit Report 2007-2016

Chapter 5. Management of fixed assets

Conclusion

The Gazelle District Development Authority (GDDA) did not maintain

proper records of

fixed assets. The assets themselves were also not properly

maintained, or managed, as

required by the Public Finance Management Act on Asset Management.

The lack of

maintaining and updating an asset register creates the potential of

mismanagement and

theft of GDDA assets.The East New Britain Provincial Government Transport Policy needs to

be reviewed, as

the policy of disposing of all vehicles after 3 years is costly and

has negative flow-on

effects to the programs of the GDDA.

Key Findings

The historical total value of all Gazelle District Development

Authority (GDDA) assets

maintained in the asset register was K10,645,103.00. However, the

asset register was -

Page 44 of 48

-

incomplete and does not capture full details of assets purchased

over the years, or their

current market value. Also, a large number of assets were either not

located or identified

as damaged during the course of the audit.In compliance with the East New Britain Provincial Government

Transport Policy, the

GDDA was to dispose of more than 45 motor vehicles (including heavy

equipment) with

a total valuation amount of K1,313,950, as they were over 3 years

old.Due to poor historical asset management data and records maintained,

the audit could

not ascertain the actual economic value of the motor vehicle fleet

as at current date of

disposal. It was also noted that some of the vehicles that were to

be disposed of were not

even registered in the asset register that was maintained at the

GDDA.Chapter 5 Findings

Asset Management

5.1 The historical total value of assets maintained in the asset

register records was

K10,645,103.00. The audit found that the asset control

environment for Gazelle

District Development Authority was generally weak.

5.2 The audit noted that the records in the asset register were

incomplete. For

instance, a long base Hino Truck purchased in 2016 at a cost of

K92,500.00 was

not captured in the asset register records. Other assets such as

laptops or

cameras were not captured in the asset register.

5.3 There was no stock-take of assets conducted annually to verify

their existence

or the condition of the assets. The ‘wear and tear’ costs

(Depreciation Cost) of

the assets was not reflected in the register, so the market value

as at a current

date could not be determined.41 | Gazelle DSIP Performance Audit Report 2007-2016

ENB Provincial Transport Policy requires Government Vehicles and

assets to be

disposed of after 3 years.

5.4 The ENB Provincial Transport Policy requires Government

Vehicles and assets -

Page 45 of 48

-

to be disposed of after 3 years. In line with this policy, the

GDDA disposed of a

total of 45 vehicles (including heavy equipment) with a total

valuation amount

of K1,313,950.00. According to the Tender documents, the disposal

was

undertaken through an approval by Board of Survey (BOS) in 2016.

5.5 Due to the poor historical asset management data and records

maintained, the

audit could not ascertain the actual economic value of these

vehicles as at the

date of disposal. It was also noted that some of the vehicles

that were to be

disposed of were not listed in the asset register.

Vehicle replacement will put a strain on DSIP funds that is meant

for service

delivery

5.6 The ENB Provincial Transport Policy should be reviewed.

Disposing of a large

number of vehicles at the same time, significantly affects the

ability of staff to

travel for work purposes. Furthermore, it is very costly to

replace vehicles after

only 3 years. With development funds ceiling being reduced each

year,

constantly purchasing vehicles and machinery will put pressure on

the limited

funds available for programs.

Figure 12: Images of the 48 GDDA vehicles that were pooled to be

disposed of in accordance

with the ENB Transport Policy to replace vehicles after 3 years -

Page 46 of 48

-

42 | Gazelle D S I P Performance Audit Report 2007-2016

Recommendation 5

AGO recommends that the Gazelle District Development Authority

(GGDA):

1. Undertake a stocktake of all government assets, building, plant,

equipment

vehicles furniture’s and fittings, and a centralised asset

management system is

developed and maintained by a dedicated officer to ensure that

all assets are

accounted for.

2. Have a dialogue with the East New Britain (ENB) Provincial

Administration to

review the policy for disposing of vehicles after 3 years. This

is a costly exercise

and the GDDA has no budget for buying new vehicles or machinery

for the

DSIP sectoral programs.

Response

Gazelle District Development Authority agreed with findings. -

Page 47 of 48

-

43 | Gazelle D S I P Performance Audit Report 2007-2016

Appendixes

List of TablesTable 1: Distribution of DSIP K10 million through sectors 2013-2016

16

Table 2: Total DSIP Funds allocated and Released to Gazelle District

16

Table 3: Summary of payments made as token of appreciation for years

2015 & 201625

Table 4: Total Wages paid from the District Treasury Operating

Account 26

Table 5: Total Paid as school fee’s assistance for years 2015 & 2016

28List of Figures

Figure 1: Gazelle District Development Authority (GDDA) Financial

Records stacked

outside the GDDA treasury office

18

Figure 2: DSIP revenue vs Expenditure in Gazelle District from 2013

to 2016. 21

Figure 3: DSIP Expenditure by sector in Gazelle District for years

2013-2016 22

Figure 4: Some of the GDRMU machinery that needs maintenance and

replacement.28

Figure 5: Vuvurai Road less than 300meters resealed for K1.8 million

32

Figure 6: Image of the empty space taken in November 2017 where the

proposed

K3Million Kerevat Market was to have been built.

33

Figure 7: Image shows the empty space and the fencing for Tokiala

Fibre Glass,

taken in November 2017

34

Figure 8: Utmei Aidpost left unfinished and unoccupied due to

incomplete

infrastructure and bad planning.

35

Figure 9: Vunapalading Uncomplete Construction of the Kerevat Health

Hospital

Oncall Nurses Duplex

37 -

Page 48 of 48

-

Figure 10: Current Facility used by on call nurses at Kerevat Rural

Hospital. A

makeshift store-room converted to sleeping room.

38

Figure 11:Image of the incomplete X-ray room

39

Figure 12: Images of the 48 GDDA vehicles that were pooled to be

disposed of in

accordance with the ENB Transport Policy to replace vehicles after 3

years 4244 | Gazelle D S I P Performance Audit Report 2007-2016